Set Rules Once, Apply Everywhere: Smart Policy Enforcement Across Payment Channels

In today’s omnichannel financial ecosystem, businesses in Kenya and beyond are confronted with a variety of payment methods—mobile money, bank transfers, corporate cards, petty cash, virtual wallets, and more. While this diversity offers flexibility, it also presents a significant challenge: how to enforce consistent spending policies across all channels.

.jpg)

The core principle is simple: define your policies once and let them apply across every payment channel, ensuring seamless compliance, clearer oversight, and streamlined workflows—no matter how money moves. Here's why this approach is transformative.

The Activation Challenge: Multiple Channels, Siloed Controls

Consider a typical medium-sized enterprise in Nairobi today:

- Sales agents receive travel allowances via M-Pesa.

- Office rent and vendor payments go through bank transfers.

- Marketing teams use corporate virtual cards.

- Field agents rely on petty cash for on-the-go expenses.

Each channel is managed separately—M-Pesa logs, bank statements, card portals, spreadsheets, and handwritten petty cash receipts. This fragmentation has critical downsides:

- Delayed reconciliation: Finance teams are forced to manually gather and cross-check disparate data.

- Policy slippage: Different channels can mute consistent spend controls.

- Compliance risk: Inconsistent receipt capture and approval flows increase fraud potential.

PwC’s 2020 Kenya Fraud Survey reported that 44% of companies experienced economic crime, with internal operations staff responsible for 53% of incidents, often exploiting weak internal controls

A Unified Policy Layer: One Definition, All Channels

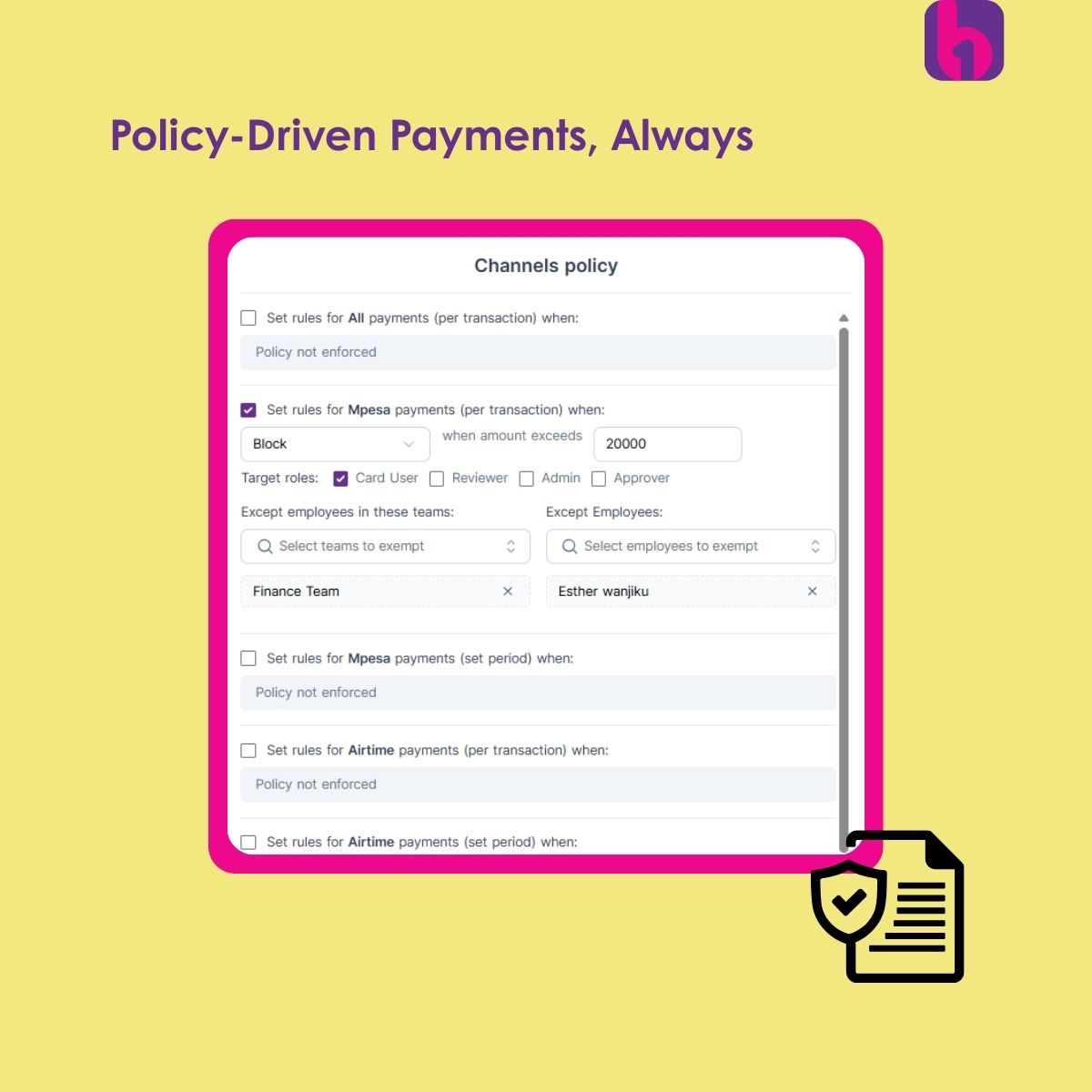

By adopting a centralized policy engine, businesses can specify spend rules—who can spend, how much, for what purpose, and via which channel—and automatically enforce them across the board:

- Create mobile-wallet limits: Field agents only see a weekly M-Pesa allowance, with strict entry validation.

- Issue virtual cards with real-time caps: Team leads get cards restricted to online ad spend or software subscriptions.

- Cash-out rules: For petty cash, employees pre-declare expenses; receipts are submitted via mobile app before disbursement.

This eliminates fragmented manual oversight and makes policies central to all payments—no more piecemeal approvals channel-by-channel.

Real-Time Visibility & Automated Controls

With real-time transaction aggregation and policy enforcement:

- Live dashboards show current spend by channel, team, and vendor.

- Automatic alerts trigger when someone exceeds their limit or uses an unauthorized channel.

- Receipts are snapped and matched upon transaction completion, transforming paperwork into digital records.

Enhanced Compliance and Fraud Prevention

With everything flowing through a centralized platform:

- Every transaction is tagged with user, purpose, channel, and project.

- Approval histories and audit logs are searchable and immutable.

- Exceptions and anomalies trigger investigations.

As PwC’s data indicates, internal fraud tends to occur where controls are weakest. By enforcing unified rules and maintaining transparent logs, companies dramatically reduce both accidental overspend and deliberate misuse.

Scaling Made Simple—Grow Without Growing Pains

As companies expand—adding branches, field agents, departments, or project teams—the complexity increases:

- More payment channels emerge.

- Different teams require unique spend rules.

- Remote and field-based staff complicate reconciliation.

Centralized policy enforcement scales effortlessly. Policy configurations can be cloned or tweaked for new teams. Channels are added to the same framework, simplifying onboarding and oversight.

This echoes what Boya describes as “multichannel expense management”: a unified dashboard that pulls in M-Pesa, bank, card, and petty-cash transactions—all accessible via filters on team, vendor, method, or time.

A Kenyan Case Study: Why Multichannel Expense Management Matters

As outlined in our recent blog “Why Multichannel Expense Management Is the Future of Finance in Kenya”, Kenyan businesses commonly juggle MPESA payments, bank transfers, cards, and cash, yet manage each with fragmented systems—leading to delayed reconciliations, lost receipts, and lack of policy consistency.

By implementing a multichannel platform like Boya, companies:

- Centralize transactions in one view.

- Capture transactions and receipts in real-time.

- Enforce spend policies across channels like M-Pesa allowances, virtual card limits, and petty cash rules.

The result: fewer errors, faster approvals, improved budget control, and a complete audit trail—what every modern finance function needs.

Building Your Smart Policy Framework

To operationalize “set once, apply everywhere,” follow this roadmap:

- Map all payment flows: Identify every channel your company uses—M-Pesa, cards, transfers, cash, wallets.

- Define core rules:

- Role-based limits per channel

- Allowable categories (travel, subs, procurement)

- Required approvals and receipt requirements

- Role-based limits per channel

- Select a platform: Choose a provider that integrates all channels, provides real-time dashboards, supports policy workflows, and includes mobile receipt uploads.

- Test with pilot teams: Configure policies, run pilot cohorts, gather feedback, and refine.

- Scale & monitor: Roll out in phases while monitoring compliance, approving anomalies, and adjusting thresholds.

- Audit regularly: Use transparency and logs to detect unauthorized changes or unusual override patterns.

Summary: Why It Matters

- Consistency: Spend rules are uniform—no matter how the money moves.

- Efficiency: Finance teams save hundreds of hours monthly.

- Accountability: Users know what they can spend, where, and how.

- Scalability: Roll out smoothly across new teams and channels.

- Compliance: Audit-ready records and real-time alerts.

- Fraud reduction: Centralized enforcement reduces internal threats.

Final Thoughts

The era of siloed expense systems is ending. Businesses must adapt to smart, policy-driven spending across multiple payment channels—from M-Pesa and bank transfers to virtual cards and petty cash. “Set rules once, apply everywhere” isn’t just a mantra; it’s a strategy for unlocking efficiency, accountability, and financial clarity.

Ready to move beyond manual and fragmented policies?

Explore how Boya can help your business take control of expenses across every channel. Visit BoyaHQ.com